.png)

Bel20 index peaks eighteen years after previous record

The Brussels Stock Exchange's Bel20 index set a record last week, no less than eighteen years after the previous one. A reason to celebrate is not. The index has its merits, but certainly also its shortcomings, as its history shows.

Last Friday, the Bel20 - the index of Belgium's top 20 listed companies - tapped a record price at 4,796 points. The previous record dated from May 2007. Trends asked some analysts and fund managers, together accounting for more than a century of experience in Belgian equities, about the trajectory of the Belgian index over the past 20 years and the significance of that record.

The Bel20 dipped from a high of 4,757 points in May 2007 to a low of 1,527 points in March 2009. Other European and especially U.S. indices climbed out of the valley much faster after the 2008 financial crisis. The American S&P500 took five and a half years, the German DAX just under six years. The Dutch and French stock market indexes went through their pre-crisis records in 2021.

Wrong mix

Consequently, the financial crisis hit the Belgian star index harder. "At the time, KBC, Fortis and Dexia together had a considerable weight in the index. Those financial institutions all went down heavily and that made a quick recovery difficult. KBC survived and is now one of the better capitalized and most profitable banks in Europe. Dexia disappeared, Fortis barely survived and later became Ageas," says Patrick Millecam, manager of the Belgian equity fund, among others, at independent asset manager Value Square. KBC only recently broke through its 2007 record price. Ageas is still trading at a fraction of the prices of the late Fortis.

Brewer AB InBev, accounting for an index weight of 10 to 12 percent, put the brakes on price appreciation over the last decade. "If such a heavyweight doesn't do well, then the index can't make high peaks either," he said. Since its acquisition of SAB Miller, the beer giant has struggled with excessive debt. Free cash flow flow flowed mostly to debt reduction and not to shareholders," said Patrick Vermeulen, asset manager at Ascot House. In addition, the Bel20 missed the sectors that excelled. "The index is heavily focused on traditional value stocks with more limited growth potential but high dividends, which weighs on the index's share price. Unlike other indexes, such as the S&P500, the Bel20 lacks high-growth sectors, such as technology, defense and luxury," said Wim Lewi, head of equity research at KBC Securities.

The same, yet different

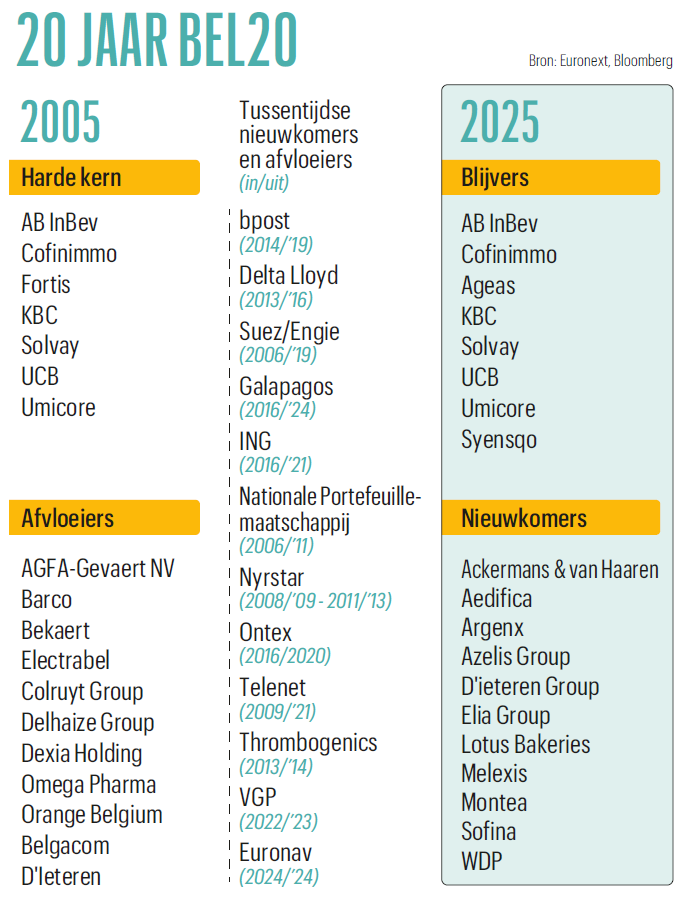

Has the Bel20 changed much in those 20 years? Yes and no, it sounds. "At least it is better diversified across sectors," says Patrick Millecam. Nine companies are the same as in 2006 - 10, if we include Syensqo as a sister company of Solvay. "Those stayers account for 65 percent of the index weight. The big blocks haven't changed much. Among the newcomers are a number of stock market successes of recent years, such as argenx, Melexis and Lotus. And with WDP, Aedifica and Montea, there is much more real estate in the Bel20 than there was two decades ago," the Value-Square manager adds.

On the flip side, the index once included such failures as Agfa-Gevaert, bpost, Galapagos, Ontex and Nyrstar, in addition to a number of run-offs, such as Barco, Orange, Delhaize, Colruyt and Bekaert.

Holdings or investment companies now weigh heavily in the Bel20. In 2006, it was only GBL of the late Albert Frère. A year later it was joined by Ackermans & van Haaren, and still later by Sofina and D'ieteren. "Do they even have a place in such an index?" wonders Patrick Vermeulen. "They are investment vehicles of the controlling families, without an industrial activity of their own. British stock market indexes do not include such investment funds. You can still defend the place of D'Ieteren and Ackermans & van Haaren, because they are co-directors of the companies in which they invest."

Composition needs to be more dynamic

A stock index performs only as well as the underlying stocks. So the composition is decisive, but it follows rules about freely tradable stocks and market capitalization, among other things. "The composition changes too slowly. A company has to do well for years before it can win a seat in the Bel20. A lot of upside potential has already been realized at that point," says Patrick Vermeulen, giving Lotus Bakeries as an example. "The cookie maker put in fantastic performances, but due to limited trading volumes, a Bel20 seat was not possible for a long time. The company was actually punished because it has loyal shareholders. When Lotus finally hit the Bel20, the stock took hits in the wake of a temporary slowdown in growth."

Patrick Millecam, in turn, gives chip developer Melexis as an example. "We look annually at which stock market companies achieve the greatest value creation, and Melexis has been in the top three for ten years. But the stock had already risen significantly when it finally got into the Bel20," he says. "In 2021, it got in at a price of 84 euros. A year after that it went out at 83, to get back in in 2023 at 100 euros. Currently, the share costs about 67 euros. Investors hoping to benefit from the stock market performance of Melexis via the Bel20 are in for a treat. While the stock has posted an annual return of 16 percent since its IPO in 2002, compared to 4.5 percent for the Bel20 over the same period."

The composition rules also work against the index's performance in reverse, Patrick Vermeulen adds. "It also takes a long time for a company to lose its seat. Weak brothers stay in charge for a long time, instead of clearing the field for promising companies," he says. "It's also not obvious to replace dying stars. For that, you need a dozen or so new promising companies, but fresh blood is scarce. Such companies are also more likely to seek financing on private markets or in the U.S. With D'Ieteren, Sofina, Lotus and Elia we have strong companies in the index, but they are no substitutes for an AB InBev with a market capitalization of almost 100 billion euros," also says Kris Kippers, head of equity research at Degroof Petercam.

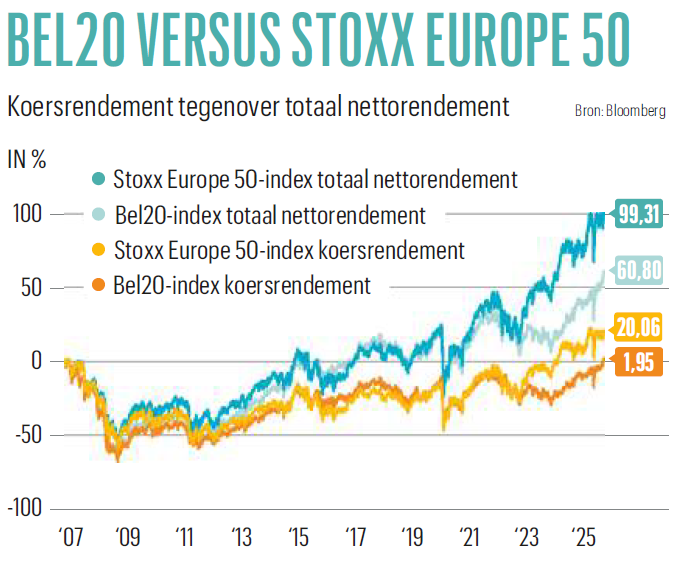

20 is too little, but more is not better

This raises the question of the relevance of the Bel20. Patrick Millecam cautions against taking the Bel20 an sich as a gauge of Belgian stock market performance. "Many Belgian stock market companies pay dividends. You have to add those to the price return. That gives a more accurate and honest picture," he says. The total net return - being stock price performance plus dividends minus dividend taxes - of the Bel20 since 2007 is 60 percent. That's not outrageously lower than the Stoxx Europe 50's 90 percent. "Thanks to the very strong performance of a number of European banks and outliers like Siemens and Airbus, the latter in particular has been doing much better since the end of 2022," he says. Real estate companies in the Bel20 have been weighing on the evolution since 2022 due to increased interest rates," said Patrick Millecam.

Since its creation in 1991, the Bel20's total return - price evolution plus dividends - has averaged 8 percent per year. The number of companies in the Belgian star index is also questionable. "Twenty companies as the basis for an index is few. The concentration is high, so company-specific developments have a big impact on the whole," says Patrick Vermeulen. The largest ten companies in the Bel20 account for 75 percent of the index weight. Gut feeling would say that the Belgian All Shares, with its 116 companies, is a better alternative. "But that's not true," says Patrick Millecam. "There, too, the top ten account for 75 percent of the weight, just as in the Bel20. Moreover, only 53 percent of Bel All Shares companies are truly Belgian. The rest are shares of companies that were once Belgian, but were sold to foreign players who kept the listing in Brussels. Albert Frère was the driving force behind that, for example with the sale of Petrofina to Total Energies. That makes up 17 percent of the Bell All Shares."

Moreover, the All Shares has not done much better than the Bel20. "Its total net return since 2007 is 71 percent, compared to 60 percent for the Bel20," Millecam adds.

Wim Lewi also points to external changes that have affected the Bel20 in recent years. "The index used to have more prestige, when institutional investors focused more on individual countries. In addition, there are far fewer derivatives, such as options and futures, associated with the Bel20, which therefore has less prestige," he says.

Wanted: Belgian stock market gauge

Indices are the yardsticks against which fund managers measure their performance. But the Belgian indexes fall short of that. "The top four of the Bel20 have a weighting of 46 percent. For fund managers, that is way too high, because they are only allowed to invest a limited percentage of their portfolio in one share," says Kris Kippers. "Most Bel20 companies have too low a market capitalization and marketability to be of interest to fund managers. Outside the top seven, the other Bel20s are actually small- and mid-caps, at least in the eyes of Anglo-Saxon investors. Aedifica and Cofinimmo are merging to improve their attractiveness to large investors." Also according to Patrick Millecam, the liquidity of the shares in an index is more important than the number of shares that make it up. "According to the rules, a stock cannot make up more than 10 percent of a fund portfolio and all positions higher than 5 percent cannot exceed 40 percent combined. Stocks must also be sufficiently liquid, to get in and out quickly enough. Therefore, for Belgian fund managers, no index is suitable as a reference," he says.

The smallest fund with only Belgian stocks has 40 million euros under management. Of the 110 Belgian shares, only 23 are sufficiently liquid to get in or out in

one day. For 18 shares, it would take one to five days. So for the smallest Belgian equity fund, only about 40 shares qualify for investment. The larger the fund, the smaller the choice becomes. That is also why the larger Belgian equity funds lean closer to the Bel20 index, which contains the larger liquid names. As a result, the landscape of funds investing only in Belgian equities has changed significantly over the past 20 years.

"In 2007 there were still 30 such funds, with a total of 3 billion euros under management. All the major banks then had several, along with a lot of smaller independent players. Now there are seven, together managing 560 million euros. That's 0.18 percent of the assets of all investment funds on the market in Belgium," says Patrick Millecam.

Finally, the question remains whether the Bel20 will stop at this record. "It may herald a rediscovery of the index. The strong performance of biotech and European banks could push the index higher. Although much will depend on geopolitical tensions and the evolution of interest rates," said Wim Lewi.

References:

Source: Trends

Link: https://trends.knack.be/beleggen/het-lelijke-eendje-boekt-eindelijk-nog-eens-een-record-bel20-piekt/

Authors: Jef Poortmans and Daan Killemans

Date: 21/08/2025