In shadow of tech violence, small U.S. stocks also break records

The Russell 2000, the main US index for small stocks, has bitten a record for the first time since 2021. That's a boost in a market dominated by big tech giants .

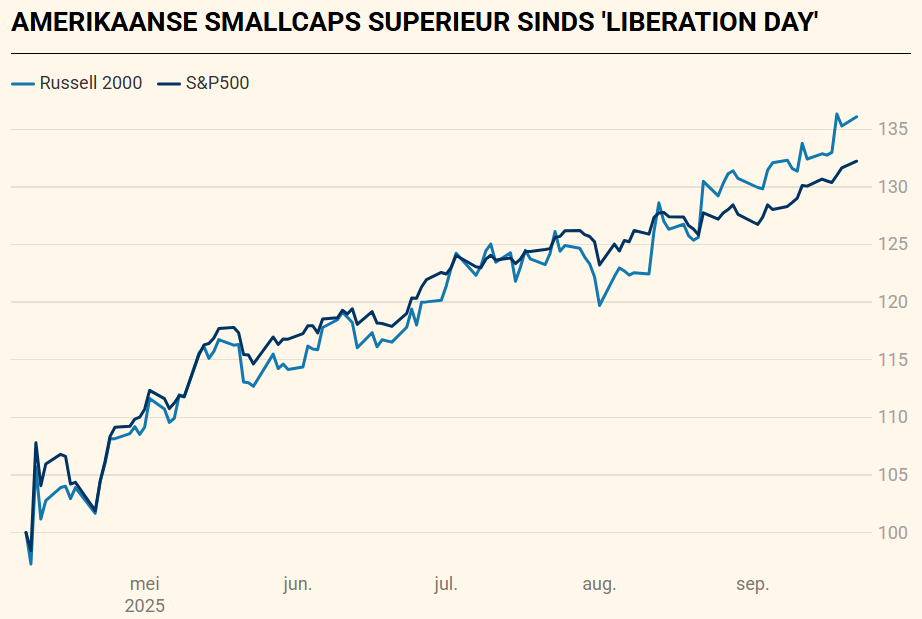

While major U.S. indexes are stringing together records, U.S. stocks with smaller market capitalizations are also doing very well. The Russell 2000, an index that tracks the performance of small U.S. stocks, also quietly reached a record high. This ends a four-year waiting period. Since the bottom after Liberation Day on April 2, the index is up more than 36 percent, measured in dollars. That beats the S&P500 (+32%).

Among the 100 most traded shares on the pan-European exchange, four more Belgian ones stand out: AB InBev (at 39 between Safran and Campari), Argenx (73), UCB (82) and KBC (93). The share of Dutch chip machine builder ASML is the only one to record more than 4 million transactions on Euronext.

The Federal Reserve's rate cut on Sept. 17 was a decisive catalyst. For small caps, interest rate decisions weigh more heavily than any other factor. The Fed cut policy rates to 4 to 4.25 percent, and the market is counting on two more cuts this year. That creates a more favorable environment for smaller companies, which are more sensitive to financing costs. In addition, they benefit from U.S. President Donald Trump's tax cuts. These particularly benefit companies with operations domestically.

Still, the relative lag remains large. Compared to the Russell 1000 (an index of larger companies) and the Russell Top 50 (the megacaps), the small-cap index has been performing weaker for years.

Sustainable rally?

The question is whether the advance is sustainable and whether the broad market can finally benefit along in a stock market dominated by large tech companies. With new interest rate cuts - expected but not guaranteed - the rally may persist, strategists believe, although that will not be true for all smallcaps. 'Cycles of interest rate cuts especially favor the higher-quality smallcaps: companies with healthy balance sheets and often the bigger names within the Russell 2000,' said Jill Carey Hall, a strategist at Bank of America.

Cycles of interest rate cuts especially favor the higher quality smallcaps: companies with healthy balance sheets and often the bigger names within the Russell 2000. - Jill Carey Hall (Startege bank of America)

HSBC points out that half of corporate debt in the Russell 2000 is variable, compared with only 10 percent in the S&P 500. So interest rate cuts are a direct windfall , but the same is true the other way around when interest rates rise. Moreover, 40 percent of companies in the Russell 2000 are loss-making, especially in unprofitable tech and early biotech.

Belgian investors looking to invest in the Russell can do so through several ETFs listed on European exchanges. The spread within the index is huge. Some companies have a market capitalization of barely $100 million to $150 million, while for the largest it is around $7 billion to $8 billion. The average market capitalization of a Russell 2000 company is $1.3 to $1.5 billion, with a median of around $700 to $800 million.

European counterparts

Contrasting that with European companies, one notices that U.S. smallcaps are often larger than their European counterparts. On Euronext, in the BEL Small or in the German SDAX, many companies move in a range of 200 to 800 million euro market capitalization.

Companies above 2 billion euros are quickly considered midcap in Europe, while in the U.S. they can still fall under the umbrella of the Russell 2000. In Belgium or the Netherlands, for example, a market capitalization of 5 billion euros is often already considered a largecap, while in the U.S. it is still a midcap.

MSCI's European small-cap index has already gained more than 9 percent this year. The basket containing 836 European companies is still trading 5.4 percent below its 2021 peak. The index trades at a steep discount to its U.S. counterpart. While the Russell 2000 is quoting at an expected P/E ratio of about 25, MSCI Europe Small Cap shares are trading around 14 times expected earnings. That means European smallcaps are on average about 44 percent cheaper than their U.S. counterparts.

References

- Source: The Time

- Link: In shadow of tech violence, small US stocks also break records | De Tijd

- Author: Christophe De Rijkce

- Photo: Fed Chairman Jerome Powell. Last week's U.S. rate cut was an additional catalyst for smallcaps. ©REUTERS

- Date: 23/09/2025